Basic tax information related to starting up business in Japan

1. Tax at the time of establishment

To open a business, there are some taxes you need to pay at the time of establishment like:

Stamp duty for KK registration: \150,000

2. Other tax matters at the time of establishment

Register your company, and then, report method of filing tax returns, method of inventory valuation, method of depreciations to director of the Tax office and metropolitan tax office. Also, you need to turn in documents such as tax report for commencement of payroll and tax report for election of consumption taxpayer.

3. Fiscal Year

II. The beginning of fiscal year for corporations in Japan can be set from any time of the year. Most corporations in Japan choose the 1st of April.

Basic tax information related with non-Japanese Individuals and non-Japanese Companies

III. Japan is one of the countries where levies include the highest corporate tax rate in the world. Now the government is planning to lower the effective corporate tax to less than 30 percent in 2016.

Source from THE WORLD BANK and Avalara VATlive

IV. What are the things to know regarding tax as non-Japanese who does business in Japan?

Source from “Comprehensive Handbook of Japanese Taxes 2006” TAX BUREAU, MINISTRY OF FINANCE

Individual (for yourself and your employee)

Taxpayer categories

Taxable income by taxpayer category

Tax returns

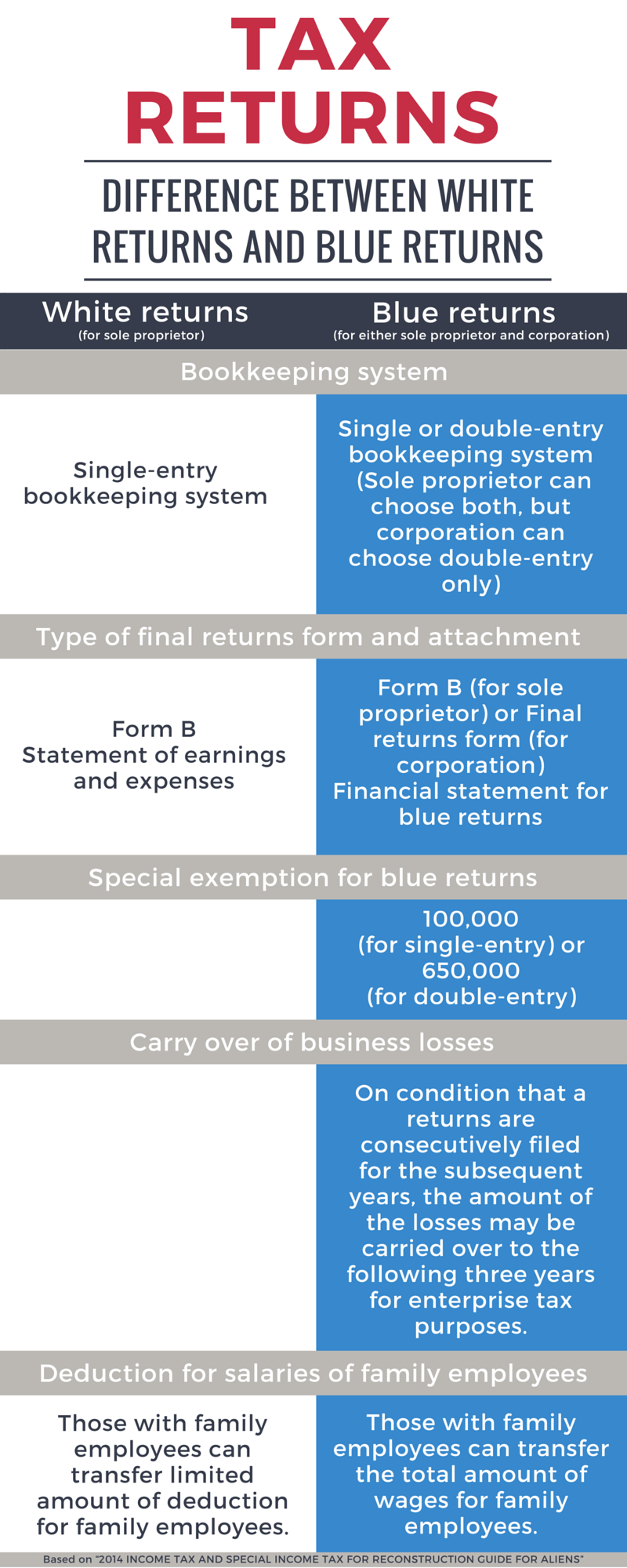

Difference between White Returns and Blue Returns

Withholding tax

Withholding tax system is used for salaries. Employer will be the one to withhold the amount of tax from the salary of the employee and pay the tax by the 10th of the following month. But the are rules for the withholding tax system is somehow very complicated, so it is better to ask a tax accountant who specializes in international taxation.

Consumption tax

Consumption tax is taxed to everyone and imposed on consumption in general in Japan. The following is what it is written about “Taxable Person” in National tax Agency Japan.

Business which falls under either of the following categories is a “Taxable Person” who is required to file the final return.

(1) Businesses which had a taxable sales amounting to more than 10million yen during the Base Period,

(2) Businesses which do not fall under category (1) above but have submitted the “Report on the Selection of Taxable Proprietor Status for Consumption Tax”, or

(3) Businesses which do not fall under category (1) and (2) above and whose taxable sales for Specified Period exceeds 10 million yen (Specified Period is in principle the first six-month of the preceding year before the Tax Period. “10 million yen” for a Specified Period can be judged by using the total amount of salary and related payments instead of using the amount of taxable sales.

Internet makes our world more complicated regarding taxation. New law and regulations are issued every year. The figure below is newly released revision of consumption taxation.

“Cross border supplies of electronic service”

Source from National Tax Agency Japan “Revision of Consumption Taxation on Cross-border Supplies of Services”

Tax treaties

Most countries now have treaties between countries. The purpose of which are listed below.

Avoidance of double taxation – Foreign tax credit

Prevention of tax evasion – Transfer pricing taxation

The Ministry of finance Japan gives you the list of countries that have tax treaties between Japan.

There are 64 conventions, applicable to 95 jurisdictions; as of December 1, 2015.

Source: Ministry of Finance Japan